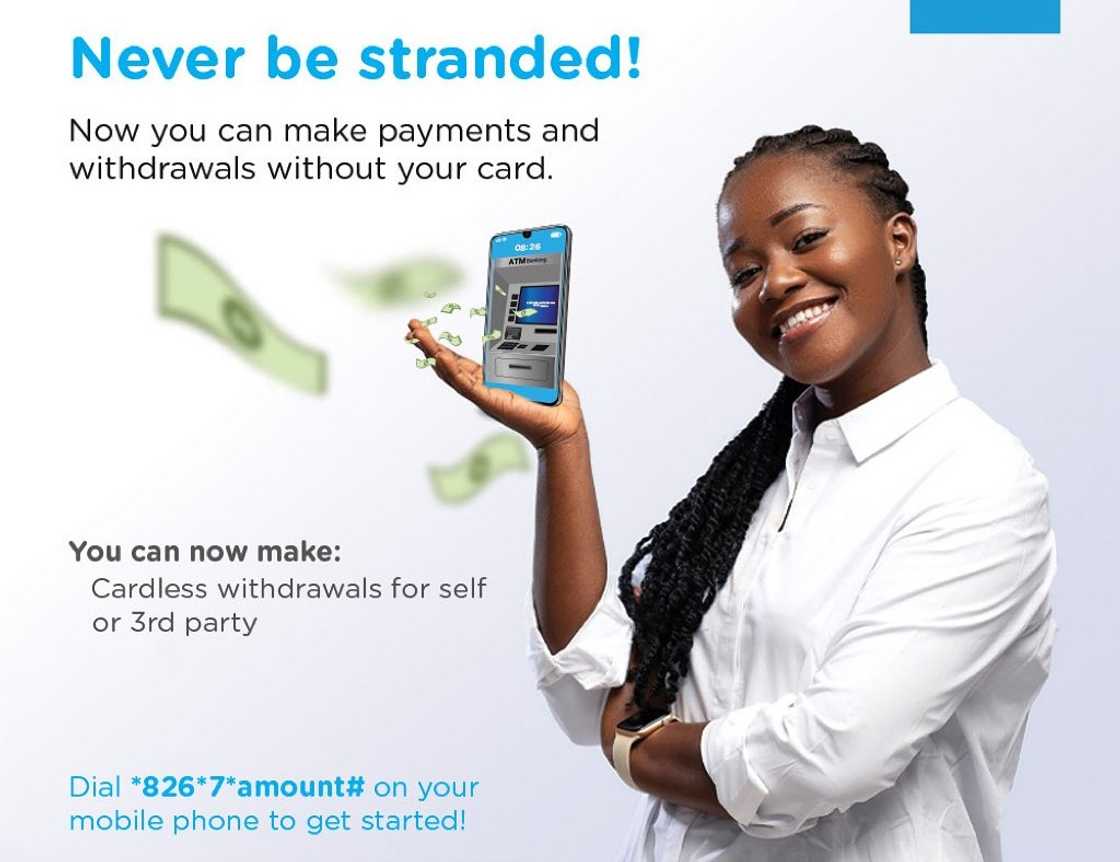

Union Bank’s *826# USSD Code: A Lifeline for Nigeria’s Unbanked and a Test of Digital Resilience

The Report

As reported by Legit.ng, Union Bank of Nigeria PLC, one of the nation’s oldest financial institutions, continues to rely on its USSD code *826# as a primary channel for offline banking. The article, a comprehensive guide, details the full suite of services accessible via the code, including money transfers, airtime purchases, balance inquiries, cardless withdrawals, and loan requests. The report emphasizes that the service is available 24/7 across all major Nigerian networks—MTN, Airtel, Glo, and 9mobile—and requires no internet connection, only a mobile number linked to the customer’s account.

The primary Union Bank USSD code is *826#. You can transfer money to Union Bank via *826*1*Amount*Account No# and to other banks via *826*2*Amount*Account No#.

The guide also outlines a daily transfer limit of ₦5,000,000 for users who increase it via the UnionOnline self-service portal, and provides troubleshooting steps for common issues such as poor network signal or insufficient session fees. The article concludes with contact information for UnionCare, WhatsApp, and email support.

WANA Regional Analysis

Against the backdrop of Nigeria’s persistent digital divide, where smartphone penetration hovers around 40% and data costs remain a barrier for millions, the Union Bank USSD code *826# is not merely a convenience—it is a critical infrastructure for financial inclusion. The broader implications for the ECOWAS region suggest that USSD banking remains the most resilient channel for reaching the unbanked and underbanked populations, particularly in rural and conflict-affected zones where internet connectivity is sporadic or non-existent.

However, the reliance on USSD technology also exposes systemic vulnerabilities. The recent spate of network outages across Nigerian telecom operators, coupled with the Central Bank of Nigeria’s (CBN) push for a cashless economy, places immense pressure on these shortcodes. Any disruption to the *826# service—whether due to technical glitches, regulatory changes, or cyber threats—could instantly disenfranchise millions of customers who have no alternative digital access. This is a stark reminder that while USSD codes democratize banking, they also create a single point of failure.

Furthermore, the article’s mention of a ₦5,000,000 daily transfer limit, adjustable via self-service, raises questions about security protocols. In a region where mobile money fraud is on the rise, the ability to increase transaction limits without a physical verification step could be exploited. WANA notes that the CBN’s recent guidelines on transaction limits for USSD channels, aimed at curbing fraud, may need to be revisited to balance accessibility with security.

Finally, the inclusion of loan requests via *826*41# signals a broader trend: the gamification of credit. Union Bank, like many of its peers, is leveraging USSD to offer instant micro-loans, a practice that, while empowering, also risks trapping low-income users in cycles of high-interest debt. As West Africa’s digital financial ecosystem matures, regulators and banks must collaborate to ensure that these tools serve as bridges to prosperity, not pitfalls.

Original Reporting By: Legit.ng