South Africa’s gambling industry has undergone a seismic transformation. No longer a peripheral leisure activity, it has exploded into a dominant economic force, fundamentally reshaping household spending, digital finance, and the nation’s social fabric. This surge, accelerated in the post-pandemic era, presents a complex paradox: a significant contributor to GDP and employment that simultaneously acts as a powerful extractor of household wealth, raising urgent questions about financial stability, regulatory adequacy, and social welfare.

The Staggering Scale of the Boom

Recent data paints a picture of explosive growth. According to the National Gambling Board (NGB), gross gambling revenue reached R59.3 billion in 2023/24—a 25.7% year-on-year increase and a staggering 150% rebound from the pandemic low of R23.3 billion in 2020/21. Even more telling is the total amount wagered: a colossal R1.1 trillion in 2023/24, with estimates for 2024/25 hitting R1.5 trillion. This liquidity flow is now a material component of the formal financial system.

The Digital Disruption: Betting Dethrones Casinos

The industry’s composition has been completely inverted. In 2009/10, traditional casinos held an 84% market share, with betting a mere 10%. Today, digital and sports betting reign supreme. This historic shift is powered by a perfect storm of factors:

- Mobile & Payment Integration: Seamless e-wallets, instant bank transfers, and mobile money have removed friction, enabling low-value, high-frequency bets from anywhere.

- Aggressive Marketing & Normalization: As noted, sponsorships of premier leagues like the PSL and the Springboks, and endorsements by sports icons, have blurred the lines between fandom and gambling. Algorithm-driven social media ads and influencer campaigns target specific demographics with unprecedented precision.

- Changing Consumption: For many, especially the youth, betting is not seen as traditional gambling but as a skill-based form of entertainment integrated with sports consumption.

Stats SA’s data on the personal services industry underscores this: bookmaker and online gambling income skyrocketed from R10.1 billion in 2018 to R152.6 billion in 2023.

The Household Impact: A Redistribution of Discretionary Spending

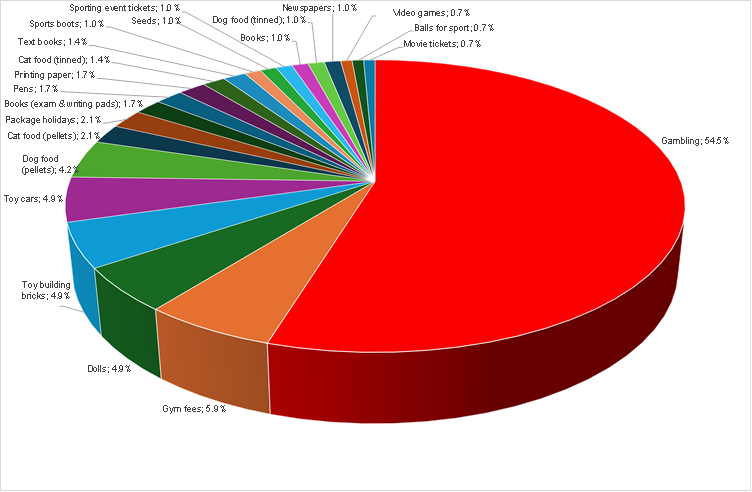

The most profound effect is on household budgets. The latest Consumer Price Index (CPI) basket revision for 2025 formally acknowledges gambling’s weight, allocating it 1.6% of total household expenditure—the 12th largest category, ahead of durable goods and just below beer. Within the “recreation, sport and culture” group, gambling now constitutes over 50% of all spending.

This signals a critical behavioural displacement. In a climate of high living costs and stagnant real wage growth, discretionary income is being reallocated from savings, durable goods, and traditional leisure toward speculative betting. This is not merely consumption; it’s a transfer of liquidity from productive or resilient uses (savings, education, home goods) to a statistically loss-making activity for the vast majority of participants.

The Macro-Financial and Social Ripple Effects

The boom creates interconnected risks and distortions:

- Financial System Liquidity vs. Household Fragility: While banks and payment processors benefit from transaction volumes, the activity channels funds away from savings and investment, potentially weakening long-term capital formation. The risk of over-indebtedness grows, particularly among vulnerable groups. Investigations revealing students using NSFAS allowances for betting exemplify this alarming trend.

- The “Extractor” Economy: The industry functions as a sophisticated liquidity extractor. It circulates vast sums (the R1.5 trillion turnover) but ultimately extracts net value (the R59.3 billion revenue) from households, often from those least able to afford it.

- Regulatory Lag Creates a Wild West: The governing National Gambling Act (2004) is woefully outdated for the digital age. A 2012 amendment to curb online advertising remains unimplemented, creating a vacuum exploited by both legal and thousands of illegal operators. This gap allows for marketing that often targets minors and avoids responsible gambling safeguards.

- Inflationary Link: Gambling’s inclusion in the CPI basket, while small, creates a novel channel for service-sector price changes to influence headline inflation, adding another layer of economic complexity.

Toward a Responsible Balance: The Path Forward

The sector’s growth is undeniable, supporting an estimated 14,000 formal jobs with spillovers into tech, advertising, and telecoms. However, sustainable economic contribution cannot be measured by turnover and tax revenue alone. The social cost of increased problem gambling, debt, and family breakdown must be factored into the calculus.

Addressing this double-edged sword requires a multi-pronged approach:

- Urgent Regulatory Modernisation: South Africa desperately needs a new regulatory framework for the digital era, encompassing strict advertising codes (especially around sports), robust age verification, deposit limits, and a unified self-exclusion registry.

- Financial Literacy as a Core Defense: Public education must move beyond generic saving advice to specifically address the mathematics of gambling odds and the recognition of problematic behaviour.

- Corporate Responsibility: Operators must be held to higher standards on data use, targeting, and intervention, moving beyond tick-box compliance to genuine harm reduction.

- Reframing the Economic Narrative: Policymakers must critically assess whether the current scale of gambling expenditure represents a healthy allocation of national income or a symptom of economic distress and diminished opportunity.

In conclusion, South Africa’s gambling boom is more than a consumer trend; it is a macroeconomic and social phenomenon reflecting digital disruption, economic strain, and regulatory failure. Without decisive intervention to prioritize household resilience over short-term revenue, the industry risks cementing a cycle of extraction that undermines the very financial stability it has come to rely on for its customer base. The nation’s challenge is to harness the innovation and revenue of this sector while erecting firm guardrails to protect its citizens from its inherent risks.

Casey Sprake is an economist at Anchor Capital.

Follow Moneyweb’s in-depth finance and business news on WhatsApp here.